The Hidden Costs of Home Ownership: What Buyers Actually Pay

Discover the expenses beyond your mortgage that every homeowner should budget for before making their purchase.

Beyond the Purchase Price

When most people think about buying a home, they focus on the mortgage payment. However, the true cost of homeownership extends far beyond that monthly mortgage bill. Many first-time buyers are shocked to discover that their actual housing expenses can be 50% higher than they initially anticipated. Understanding these hidden costs before you purchase is essential for making an informed decision and avoiding financial stress down the road.

The journey to homeownership is exciting, but it requires careful financial planning. The mortgage payment is just the tip of the iceberg. Property taxes, insurance, maintenance, utilities, and various other expenses can quickly add up, transforming what seemed like an affordable home into a significant financial burden. By educating yourself about these costs now, you can make a realistic budget and ensure that homeownership remains a positive investment rather than a financial nightmare.

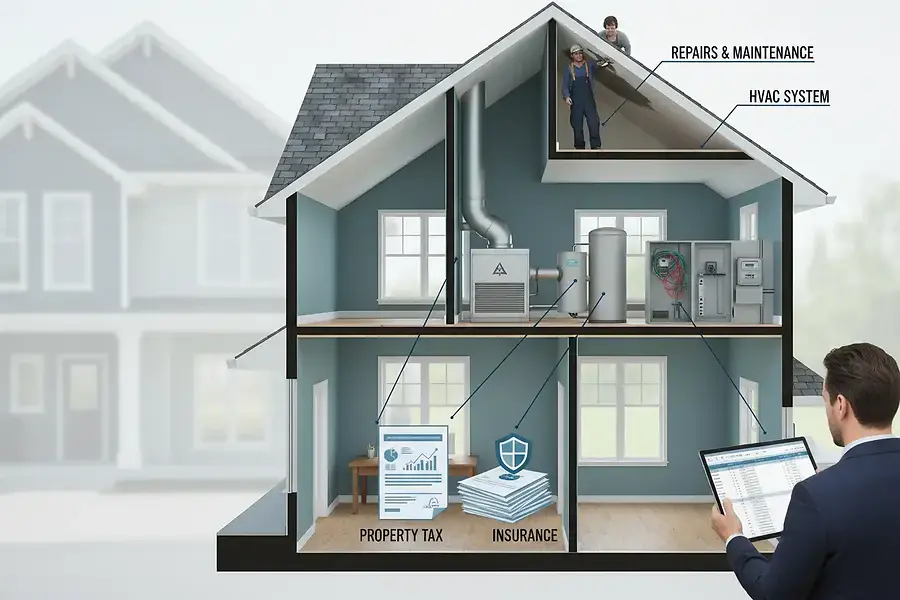

Property Taxes, Insurance, and Maintenance Expenses

Property Taxes

One of the most substantial hidden costs of homeownership is property taxes. Unlike renters, homeowners must pay annual property taxes based on their home's assessed value. These taxes vary dramatically depending on your location, with some areas charging as little as 0.3% of home value annually, while others charge over 2%. For a $400,000 home, this could mean anywhere from $1,200 to $8,000 per year in property taxes alone.

Property taxes are not fixed—they can increase over time as your home's value appreciates or as local tax rates change. It's crucial to research the property tax rates in your desired area before committing to a purchase.

Homeowners Insurance

Homeowners insurance is another mandatory expense that many buyers underestimate. Most mortgage lenders require you to carry homeowners insurance as a condition of the loan. The average homeowners insurance policy costs between $1,000 and $1,500 annually, though this varies based on your home's location, age, and condition.

Beyond standard homeowners insurance, you may also need:

- Flood insurance (required in flood-prone areas)

- Earthquake insurance (in seismic regions)

- Additional liability coverage

- Replacement cost coverage for valuable items

Maintenance and Repairs

Perhaps the most unpredictable expense is home maintenance and repairs. The general rule of thumb is to budget 1% of your home's purchase price annually for maintenance. For a $300,000 home, this means setting aside $3,000 per year for upkeep and unexpected repairs.

Common maintenance expenses include:

- HVAC system servicing and replacement

- Roof repairs and replacement

- Plumbing and electrical repairs

- Appliance repairs and replacements

- Exterior painting and landscaping

- Water heater maintenance

Older homes may require significantly more maintenance, while newer homes might have lower costs initially but could face major expenses as systems age.

Utilities, HOA Fees, and Unexpected Repairs

Utility Costs

Utility expenses are often overlooked when budgeting for homeownership. As a homeowner, you're responsible for all electricity, gas, water, sewer, and trash services. These costs can vary dramatically based on your climate, home size, and energy efficiency. In colder climates, heating costs can exceed $200-300 monthly during winter months, while air conditioning in hot regions can be equally expensive.

To reduce utility costs, consider:

- Investing in energy-efficient appliances

- Improving insulation and weatherproofing

- Installing a programmable thermostat

- Upgrading to LED lighting

- Installing solar panels (long-term investment)

HOA Fees and Community Assessments

If you're purchasing a property in a planned community, condominium, or townhome development, you'll likely face Homeowners Association (HOA) fees. These monthly or annual fees can range from $100 to over $1,000 depending on the community's amenities and services.

HOA fees typically cover:

- Common area maintenance

- Community amenities (pools, gyms, parks)

- Landscaping and snow removal

- Building insurance and repairs

- Community management

Beyond regular HOA fees, special assessments can be levied for major repairs or improvements, potentially costing thousands of dollars unexpectedly.

Unexpected Major Repairs

Even with careful budgeting, unexpected repairs can derail your finances.

A foundation crack, roof leak, or failed septic system can cost $5,000 to $50,000 or more. This is why maintaining an emergency fund specifically for home repairs is essential. Financial experts recommend keeping 3-6 months of housing expenses in reserve for unexpected emergencies.

Planning Your True Home Investment Budget

To accurately calculate your true homeownership costs, create a comprehensive budget that includes:

- Mortgage payment (principal and interest)

- Property taxes (annual amount divided by 12)

- Homeowners insurance (annual amount divided by 12)

- HOA fees (if applicable)

- Utilities (average monthly costs)

- Maintenance reserve (1% of home value annually)

- Emergency fund contributions (for unexpected repairs)

As a practical example, a homeowner with a $300,000 mortgage at 6.5% interest, living in an area with moderate property taxes and insurance, might face:

- Mortgage: $1,900/month

- Property taxes: $250/month

- Insurance: $100/month

- Utilities: $150/month

- Maintenance reserve: $250/month

- Total: $2,650/month

This is significantly higher than the mortgage payment alone and demonstrates why thorough financial planning is crucial.

Before making your home purchase, speak with a financial advisor to ensure you can comfortably afford not just the mortgage, but all associated homeownership costs. Research your specific area's property taxes and insurance rates, get a professional home inspection to identify potential maintenance issues, and build a realistic budget that accounts for all expenses.

Homeownership can be a wonderful investment and a source of pride, but only when you're financially prepared for the true costs involved. By understanding these hidden expenses now, you'll be better positioned to make a smart decision and enjoy your home without financial stress.