The Hidden Costs of Homeownership Beyond Your Monthly Mortgage

Discover the often-overlooked expenses that impact your bottom line after closing day.

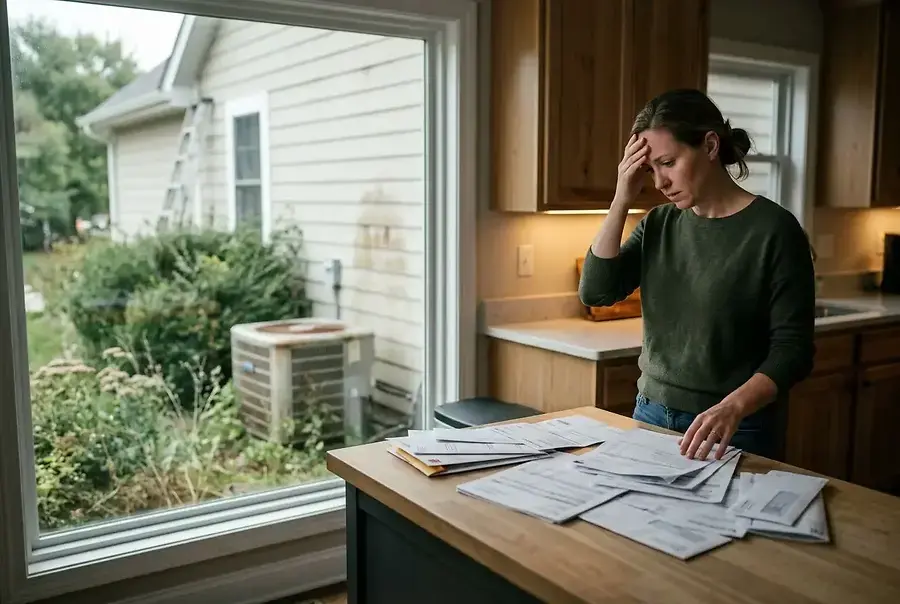

Why Most Homebuyers Are Surprised by Hidden Costs

When you finally close on your dream home, the excitement of homeownership can quickly turn to sticker shock. Many new homeowners discover that their monthly mortgage payment represents only a fraction of their true housing costs. The reality is that owning a home involves numerous expenses that extend far beyond the principal and interest you pay each month.

The problem stems from a common misconception: people often focus exclusively on whether they can afford the mortgage payment, overlooking the additional financial obligations that come with property ownership. These hidden costs can easily add 30-50% to your monthly housing expenses, catching unprepared homeowners off guard and straining their budgets.

Understanding these expenses before you buy is crucial for making an informed decision and protecting your financial health. Let's explore the major cost categories that surprise most homeowners.

Property Taxes, Insurance, and HOA Fees: The Recurring Expenses

Property Taxes

Property taxes are one of the most significant recurring costs of homeownership, yet many buyers underestimate their impact. These taxes vary dramatically depending on your location, with some areas charging substantially more than others. Property taxes can range from less than 1% to over 2% of your home's value annually, meaning a $400,000 home could cost you $4,000 to $8,000 per year in taxes alone.

What makes property taxes particularly challenging is that they typically increase over time. As your home appreciates in value, your tax bill grows accordingly. Additionally, some municipalities reassess property values periodically, which can result in sudden, significant increases in your tax obligations.

Homeowners Insurance

Your mortgage lender requires homeowners insurance, and for good reason. This essential protection typically costs between $1,000 and $2,000 annually, depending on your home's value, location, and risk factors. However, many homeowners are surprised to learn that standard policies don't cover everything.

Flood insurance, for example, requires a separate policy and can be quite expensive if your home is in a flood-prone area. Similarly, if you live in an earthquake zone, you'll need additional coverage. Don't assume your standard policy covers all potential disasters—review your coverage carefully and budget for additional protection if necessary.

HOA Fees

If you purchase a property in a homeowners association, you'll face monthly or annual HOA fees. These can range from $100 to several hundred dollars per month, depending on the community and amenities provided. HOA fees often increase annually, and special assessments can be levied for major repairs or improvements to common areas.

Before buying in an HOA community, review the budget, reserve fund status, and any planned assessments. These fees are mandatory and can significantly impact your overall housing costs.

Maintenance, Repairs, and Unexpected Emergency Costs

Routine Maintenance

Homeownership requires consistent maintenance to preserve your investment. This includes:

- HVAC system servicing and filter replacements

- Roof inspections and repairs

- Gutter cleaning and maintenance

- Plumbing inspections and repairs

- Exterior painting and siding maintenance

- Lawn care and landscaping

A common rule of thumb is to budget 1-2% of your home's purchase price annually for maintenance. For a $400,000 home, this means setting aside $4,000 to $8,000 each year for upkeep.

Major Repairs and Replacements

Beyond routine maintenance, homes eventually require major repairs and replacements. Roofs typically last 20-30 years, HVAC systems 15-20 years, and water heaters 10-15 years. When these systems fail, replacement costs can be substantial:

- Roof replacement: $8,000-$25,000+

- HVAC system replacement: $5,000-$15,000

- Water heater replacement: $1,500-$4,000

- Foundation repairs: $5,000-$50,000+

- Electrical system upgrades: $3,000-$10,000

These expenses don't follow a predictable schedule, which is why many financial advisors recommend maintaining a dedicated home repair emergency fund.

Unexpected Emergencies

No matter how well-maintained your home is, emergencies happen. A burst pipe, pest infestation, mold discovery, or structural damage can require immediate, expensive attention. Having an emergency fund of $5,000-$10,000 is essential to handle these unexpected situations without derailing your finances.

"The difference between a homeowner and a renter isn't just about building equity—it's about accepting responsibility for every system in your home. When something breaks, you're the one who pays."

Utilities and Services

While renters often have utilities included or split with landlords, homeowners bear the full cost. Budget for:

- Electricity and gas

- Water and sewer

- Internet and cable

- Trash and recycling services

- Pest control (if needed)

These costs vary by location and season but should be factored into your monthly housing budget.

Planning Ahead Protects Your Investment

The key to managing homeownership costs is preparation and planning. Before purchasing a home, take time to understand the total cost of ownership in your area. Research property tax rates, insurance costs, and typical maintenance expenses for homes similar to the one you're considering.

Create a comprehensive budget that includes:

- Mortgage payment (principal, interest, taxes, insurance)

- HOA fees and special assessments

- Routine maintenance (1-2% of home value annually)

- Emergency repair fund contributions

- Utilities and services

Additionally, consider working with a home inspector before purchase to identify potential issues that could become expensive problems. Understanding the age and condition of major systems helps you anticipate future costs and plan accordingly.

Homeownership is a rewarding investment, but it requires financial responsibility and realistic budgeting. By acknowledging and planning for these hidden costs, you'll avoid financial stress and protect your most valuable asset. The difference between struggling homeowners and successful ones often comes down to preparation—knowing what to expect and planning accordingly.

Remember, the true cost of homeownership extends far beyond your monthly mortgage payment. With proper planning and a realistic budget, you can enjoy the benefits of homeownership while maintaining financial stability.