Understanding the True Cost of Homeownership Beyond Your Mortgage Payment

Discover all the hidden expenses that impact your monthly budget as a new homeowner.

Why Purchase Price Isn't the Full Picture

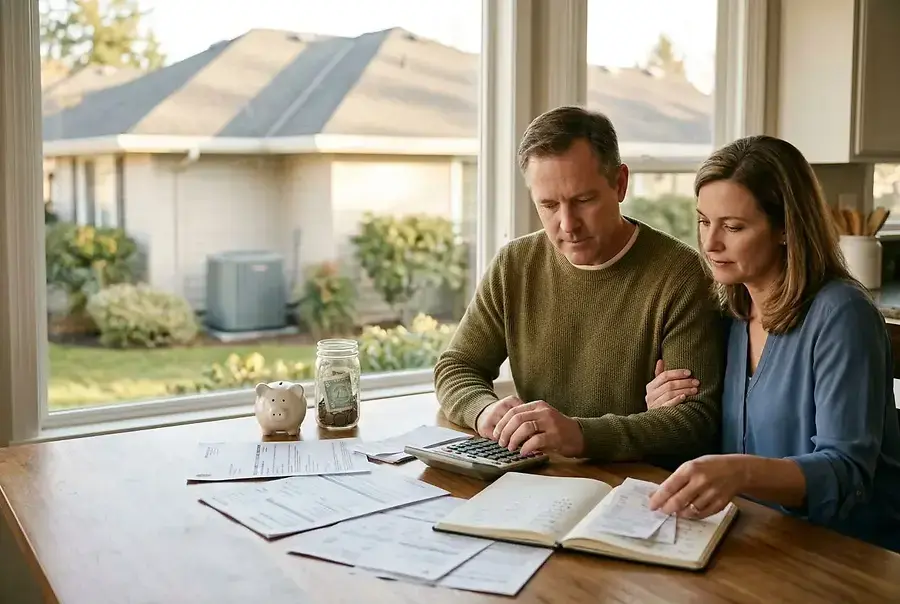

Many first-time homebuyers focus exclusively on their mortgage payment when calculating affordability, but this approach can lead to serious financial strain. The truth is that homeownership extends far beyond the principal and interest you pay each month. Understanding the complete financial picture is essential for making a sound investment and avoiding budget surprises down the road.

When you purchase a home, you're not just buying a building—you're taking on a complex set of financial responsibilities. From the moment you receive the keys, you become responsible for every aspect of the property's upkeep and operation. This shift from renting to owning represents a fundamental change in how you manage your finances.

The National Association of Realtors estimates that homeowners should budget 1-2% of their home's value annually for maintenance and repairs alone. For a $300,000 home, this translates to $3,000-$6,000 per year—money that many new owners don't anticipate.

Property Taxes, Insurance, and Maintenance: The Big Three Expenses

Property Taxes

Property taxes are one of the most significant ongoing costs of homeownership, yet they're often overlooked during the buying process. These taxes vary dramatically by location and can represent anywhere from 0.3% to 2.5% of your home's value annually. Unlike your mortgage payment, which decreases over time, property taxes typically increase year after year.

Before making an offer on a home, research the local property tax rates in your area. Ask your real estate agent for the current tax bill on the property you're considering. This information should be factored into your monthly budget calculations from day one.

Homeowners Insurance

Homeowners insurance is mandatory if you have a mortgage, and for good reason. This insurance protects your investment against fire, theft, natural disasters, and liability claims. The cost varies based on your home's location, age, construction type, and the coverage level you choose.

Don't make the mistake of choosing the cheapest policy available. Inadequate coverage can leave you vulnerable to catastrophic financial loss. Work with your insurance agent to find a policy that provides comprehensive protection at a reasonable cost.

Maintenance and Repairs

Maintenance is the third pillar of homeownership costs, and it's often the most unpredictable. Your roof, HVAC system, plumbing, and appliances all have finite lifespans. When they fail, repairs can be expensive:

- Roof replacement: $8,000-$25,000

- HVAC system replacement: $5,000-$15,000

- Water heater replacement: $1,500-$3,500

- Foundation repairs: $5,000-$50,000+

The best approach is to set aside money each month in a dedicated home maintenance fund. This creates a financial cushion for inevitable repairs and replacements.

HOA Fees, Utilities, and Unexpected Repairs: Planning for the Surprises

Homeowners Association Fees

If you purchase a property in a community with a homeowners association (HOA), you'll pay monthly or annual fees. These fees can range from $100 to over $1,000 per month, depending on the amenities and services provided. Always review the HOA budget and reserve fund before purchasing. A poorly managed HOA with insufficient reserves may face special assessments that could cost you thousands.

Utilities and Services

As a homeowner, you're responsible for all utility costs: electricity, gas, water, sewer, trash, and internet. These expenses vary seasonally and by usage patterns. A larger home typically costs more to heat and cool than an apartment. Budget generously for utilities, especially in regions with extreme weather conditions.

Unexpected Repairs and Emergencies

No matter how well you maintain your home, unexpected problems will arise. A burst pipe, electrical issue, or pest infestation can appear without warning. These emergencies often require immediate attention and can cost hundreds or thousands of dollars. Having an emergency fund separate from your regular maintenance savings is crucial for financial stability.

Pro Tip: Get a professional home inspection before purchasing and ask the inspector to estimate the remaining lifespan of major systems. This information helps you anticipate future replacement costs.

Creating a Realistic Budget and Working With Your Real Estate Agent

Building Your Complete Budget

To create a realistic homeownership budget, gather the following information:

- Mortgage payment (principal, interest, taxes, and insurance)

- HOA fees (if applicable)

- Estimated property taxes

- Homeowners insurance quotes

- Utility estimates for the area

- Home maintenance reserve (1-2% of home value annually)

- Emergency fund for unexpected repairs

Add all these expenses together to determine your true monthly homeownership cost. This number should be significantly lower than 28-30% of your gross monthly income—the standard lending ratio—to ensure you have breathing room in your budget.

Partnering With Your Real Estate Agent

An experienced real estate agent is invaluable when navigating the financial complexities of homeownership. Your agent should help you understand not just the purchase price, but the total cost of ownership. They can provide:

- Comparable property tax information for your area

- Insights into local utility costs

- Information about HOA fees and management quality

- Recommendations for home inspectors and contractors

- Guidance on negotiating repairs after inspection

Don't hesitate to ask your agent detailed questions about ongoing costs. A good agent will appreciate your diligence and help you make an informed decision.

Moving Forward With Confidence

Homeownership is one of the most rewarding investments you can make, but it requires careful financial planning. By understanding and budgeting for all the costs associated with owning a home—not just your mortgage payment—you'll be better prepared for success. Take time to research, ask questions, and work with professionals who can guide you through the process.

The key to financial stability as a homeowner is anticipating expenses before they arrive. With proper planning and realistic budgeting, you can enjoy the benefits of homeownership without the stress of unexpected financial surprises.